By Grega Horvat

When people first enter the financial markets, most of them ask the same question: “What should I buy?” Should it be stocks, gold, Bitcoin, real estate, ETFs or forex?

While choosing the right investment is important, I don’t believe it is the first question investors should ask. After more than twenty years of actively following global financial markets, I have learned that building wealth is not simply about finding the next winning trade or the next booming investment. It is about understanding that not every dollar or euro you own should have the same purpose.

Some capital should be used for active opportunities. Some should be invested patiently for years. Some should remain liquid and ready for future opportunities. Some investors may also choose to diversify into tangible assets outside traditional financial markets, such as real estate or land.

Over the years, I have realised that many traders struggle not because they cannot analyse charts, but because they approach their entire portfolio with only one mindset. Everything becomes a trade. Every market move becomes emotional. Every correction suddenly feels like a disaster.

In my opinion, that is one of the biggest mistakes investors can make.

Today, I think about wealth differently. I no longer see capital as one large account with one single purpose. Instead, I prefer to think in different buckets, each with its own objective, risk profile and time horizon. Some are designed to generate active returns, others are there to build wealth slowly, preserve capital, provide diversification or create flexibility when opportunities appear.

This article is not intended to tell you exactly how much money you should allocate to each investment. There is no perfect allocation because every investor has different goals, income, experience, age and tolerance for risk. Instead, I want to share the framework that has helped shape my own thinking over more than two decades in the markets.

Building wealth is not about finding one perfect investment. It is about giving different parts of your capital different jobs.

Trading and investing are two completely different activities

People often use the words trading and investing as if they mean the same thing. I don’t.

Although both involve financial markets, they require different objectives, different psychology and different expectations. When I am actively trading, I focus on market structure, timing and risk management. I analyse trends, sentiment, Elliott Wave patterns, support and resistance, correlations and macroeconomic developments. Every position has a predefined entry, stop-loss, invalidation level and exit strategy.

If the market proves me wrong, I move on to the next opportunity.

Investing is different. When I invest, I am not trying to predict where the market will be next week or next month. I am interested in participating in longer-term trends, allowing quality assets to appreciate over time and letting compounding do most of the heavy lifting.

The biggest difference between the two is time. A trade may last several hours, a few days or a few weeks. An investment may remain in a portfolio for years.

Unfortunately, many people mix these two approaches together. They buy something as a trade, but when the position moves against them, they suddenly decide it is now a “long-term investment”. The original trading plan disappears, stop-losses are ignored and the only reason the position remains open is because the investor hopes the market will eventually recover.

Hope, however, is not an investment strategy.

Why one account should not do everything

Another common mistake is putting every investment into one account while expecting that account to accomplish everything.

Imagine someone with €100,000 to invest. They deposit the entire amount into one trading account. Inside that account, they actively trade forex, own technology stocks, speculate in cryptocurrencies, buy commodities and occasionally open leveraged positions.

At first glance, it may appear diversified because different assets are involved. In reality, everything is still being managed with the same mindset. Every market fluctuation affects the entire portfolio. Every losing trade increases emotional pressure. Every correction suddenly feels much larger than it actually is.

I prefer thinking differently. Instead of asking, “Which market should I buy next?”, I first ask, “What job should this capital perform?”

Once you begin asking that question, portfolio construction becomes much more logical.

Think in buckets, not percentages

One question that matter is: “How much should I allocate to stocks, forex or crypto?”

My answer is usually the same. The exact percentage is not the most important decision. The purpose is.

Rather than focusing only on numbers, I find it more useful to think about different buckets within a portfolio. Each bucket has a completely different objective.

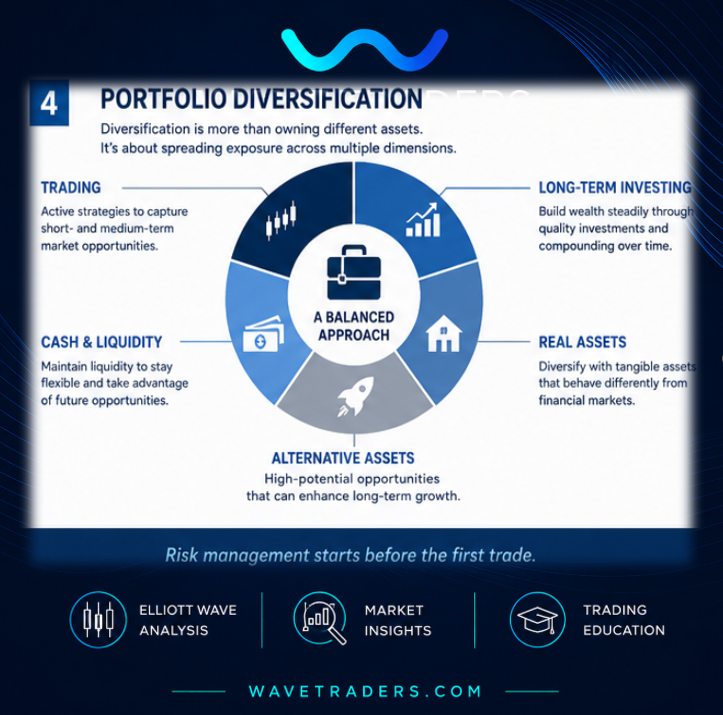

The first bucket is active trading. This is where I spend most of my day, analysing forex, indices, gold, oil, commodities and individual stocks. The objective here is not simply to own assets. It is to identify opportunities created by market structure, sentiment, technical analysis and macro conditions. Trading requires discipline, active management and the ability to accept losses. Capital allocated here should be viewed as working capital rather than long-term savings.

The second bucket is long-term investing. This serves a completely different purpose. Instead of trying to capture every market swing, I am interested in participating in broader economic growth. This may include diversified ETFs, index funds, quality companies or dividend-paying businesses. Many long-term investors also use Dollar-Cost Averaging, or DCA, where they invest a fixed amount regularly instead of trying to perfectly time every market bottom. No one consistently buys every low. DCA removes much of the emotion from investing and allows investors to gradually build positions over time. In my opinion, consistency often beats perfection.

The third bucket is real assets. Financial markets are not the only place where wealth can be built. Some investors choose to diversify part of their portfolio into tangible assets such as residential property, commercial real estate, land or physical precious metals. These investments behave differently from stocks and currencies because they are influenced by different economic forces. Real estate, for example, often follows much longer economic cycles and may provide rental income, inflation protection or diversification away from financial markets. This does not mean everyone should own property. The important lesson is that financial markets represent only one part of the investment universe.

The fourth bucket is alternative investments. Depending on experience and risk tolerance, some investors may allocate a smaller portion of capital to higher-risk opportunities such as cryptocurrencies, private investments or other speculative themes. These assets can offer strong upside, but they also carry significantly higher volatility. For that reason, I believe they should complement a portfolio rather than become its foundation.

The final bucket is cash and liquidity. Many investors underestimate this part, but I think it is extremely important.

Why cash is also an investment

Cash is often seen as “doing nothing”, especially when markets are rising and optimism is everywhere. I see it differently.

Cash is not valuable because it generates spectacular returns. It is valuable because it provides flexibility.

Markets move in cycles. There are periods when opportunities are everywhere, and there are periods when patience is far more valuable than constant activity. Having available liquidity allows investors to react when opportunities appear instead of being forced to sell existing investments at the wrong time.

Cash also reduces emotional pressure. When every cent of your wealth is invested, market corrections often feel much larger than they actually are. Investors then begin making decisions based on fear rather than logic.

Sometimes the best investment decision is simply waiting.

Cash does not mean you are bearish. It means you are prepared.

Different assets have different personalities

One of the biggest advantages of following multiple asset classes for many years is that you begin to recognise that every market behaves differently.

Stocks have their own personality. Currencies have another. Commodities often follow completely different cycles. Cryptocurrencies behave differently again. Even real estate moves according to its own long-term fundamentals.

Stocks are usually connected to earnings, economic growth, business cycles and investor confidence. Forex is heavily influenced by interest rates, central banks, inflation expectations and macroeconomic trends. Commodities are often driven by supply, demand, geopolitics and cyclical pressures. Cryptocurrencies remain highly volatile and sentiment-driven. Real estate is a tangible asset class with longer economic cycles, often influenced by interest rates, location, demographics and credit conditions.

Trying to analyse every market with exactly the same approach usually leads to frustration. Understanding these differences allows investors to become more flexible instead of forcing every market into the same framework.

Risk management starts long before you enter a trade

Whenever traders hear the phrase risk management, they usually think about stop-losses. While stop-losses are important, I believe risk management begins much earlier.

It begins before the first trade is even placed.

It starts with questions like: How much of my total capital should be allocated to active trading? How much belongs in long-term investments? Am I overexposed to one sector or asset class? How much leverage am I using? Do I have enough liquidity if markets become volatile?

These decisions have a much greater impact on long-term performance than adjusting a stop-loss by a few points.

One of the biggest advantages of separating different investment buckets is psychological. If only a portion of your capital is allocated to active trading, you naturally become more objective. Losing trades remain part of the business instead of becoming personal financial disasters.

The same applies to investing. If your long-term portfolio is separate from your trading capital, you are far less likely to panic because of short-term market noise.

Good portfolio construction makes good risk management much easier.

Diversification is more than owning different assets

Many investors believe diversification simply means owning a variety of stocks. That is one form of diversification, but I think the concept goes much further.

True diversification means spreading exposure across different sources of return, different investment horizons and different economic cycles.

For example, someone may own twenty different technology stocks and believe they are diversified. In reality, those companies may all react similarly if the technology sector experiences a major correction. Likewise, owning stocks, cryptocurrencies and leveraged forex positions inside the same trading account does not necessarily create diversification if all positions are driven by the same emotions and the same appetite for risk.

A more balanced approach considers several dimensions at the same time: asset classes, strategies, time horizons, economic cycles and liquidity.

The objective is not to eliminate risk. That is impossible. The objective is to avoid having your entire financial future depend on one decision, one asset or one market.

Building wealth is about consistency

One of the biggest misconceptions about financial markets is that wealth is created through a handful of spectacular trades.

Exceptional opportunities certainly exist, but most long-term wealth is built much more quietly. It is built through consistency: consistent investing, consistent risk management and consistent decision-making.

Compounding rarely attracts headlines because it is not exciting. Yet over decades, it remains one of the most powerful forces available to investors.

The same principle applies to trading. Successful traders are not defined by one outstanding trade. They are defined by hundreds of disciplined decisions made over many years.

The market does not reward perfection. It rewards discipline.

Protecting capital is not the opposite of making money. It is what makes long-term wealth possible.

My biggest lesson after more than twenty years

When I look back at my own journey through the financial markets, I do not think my biggest edge came from discovering one indicator or one trading strategy.

Technical analysis has certainly helped me. Elliott Wave analysis has become an important part of my work, and understanding market structure has improved my decision-making significantly. But if I had to identify one lesson that stands above everything else, it would be this:

Never allow your entire financial future to depend on one market, one account or one strategy.

Markets evolve. Opportunities change. Economic cycles come and go. Some investments perform exceptionally well for several years before entering long periods of underperformance. Others quietly build value over decades.

Trying to predict which asset class will outperform every year is incredibly difficult. Building a portfolio capable of adapting to different market environments is much more realistic.

Today, I do not see trading and investing as competing activities. I see them as complementary. Active trading allows me to take advantage of shorter-term opportunities. Long-term investing allows capital to compound. Real assets can provide another layer of diversification. Cash provides flexibility when opportunities arise.

Each bucket serves its own purpose, and together they create a framework that is far more resilient than relying on a single investment idea.

Final thoughts

There is no perfect portfolio. There is no universal allocation that works for everyone. Your financial goals, experience, income and tolerance for risk will always be different from someone else’s.

However, I do believe there is a better way to think about building wealth.

Instead of asking yourself, “What should I buy next?”, try asking a different question: “What role should this investment play within my overall portfolio?”

That simple shift changes the conversation completely.

Some investments are designed to generate income. Some are designed to preserve purchasing power. Some are there to create long-term growth. Some provide flexibility during uncertain times.

The most successful investors rarely depend on one market or one strategy. Instead, they build a framework where different assets complement one another through changing economic cycles.

Markets will continue evolving, new opportunities will emerge and unexpected challenges will always appear. You cannot control those events. What you can control is how you structure your capital, how you manage risk and how patiently you allow your long-term strategy to unfold.

For me, that is one of the most valuable lessons the markets have taught me over the last twenty years.

Thank you for reading,

Grega Horvat

Founder, WaveTraders

Disclaimer: This article is for educational purposes only and does not constitute investment advice, financial recommendations or a solicitation to buy or sell any financial instrument.